This document is a review draft. Readers are invited to submit comments to the Taxonomy Design Working Group.

Table of Contents

1 Introduction

It is expected to become more common for a single report to meet obligations to multiple data collectors or for different reporting requirements. This trend is primarily driven by the need for more efficient data collection, more informative reports and reduced reporting burdens.

In particular, efficiencies can be gained in the production of reports if they can produce a single document that covers several reporting requirements where:

- The data is the same or covers similar topics, for example, dual filing for listed companies the in US (20-F) and Europe (Annual Financial Reports);

- The disclosures are complementary and sit naturally together, for example financial and sustainability reporting; or

- Requested information and the report content overlaps, for example, GRI and ESRS data standards.

However, when setting data standards for XBRL or Inline XBRL reports, it can be easier to maintain high quality taxonomies that cover specific topics or requirements separately. This means the taxonomies will be independent of each other.

This leads to a situation where data collectors need to find a way for a single report to cover multiple reporting requirements that are often in independent taxonomies. Fortunately, the XBRL standard has multiple approaches to achieve this and this guidance is written to help make the decision on which to use.

This guidance specifically covers the case where it is beneficial, or required, for a single Inline XBRL report to target multiple different data standards or regulations. This may be to submit to one or more data collectors. It considers the perspective of standards-setters, preparers, data collectors and consumers of the resulting report, but is primarily aimed at data collectors who need to support approaches that enable single documents to be used for multiple reports.

2 Understanding the problem

The primary goal of a data collector is to ensure that they receive data from a certain group of preparers to address their specific reporting needs. Companies that prepare reports under such filing programmes are often tasked with submitting additional reports to other data collectors (or the different departments within the same data collector).

Currently, the data collectors decide whether a report meets the reporting obligation of their filing programmes. They often define restrictions which mean that preparers must meet certain filing rules or use specific taxonomies. A common restriction is that only a taxonomy from an allowed list may be included in a report. Filing rules such as these prevent preparers from using a single report for multiple collectors, even if the content of these reports overlaps or is considered as supplementing each other.

The corporate annual report is an example of a report that contains data on a number of topics (both financial and non-financial), each potentially relevant to a different audience. In particular, the introduction of sustainability data into the report is a case where a single report could meet the obligations to multiple data collectors.

Another, more process-oriented case is where a report is sent to one data collector but split out so that parts go to different agencies. We can consider this as the case where a single report is meant to meet a single obligation covering multiple topics.

3 Mechanisms offered by the standard

The XBRL standard is flexible in terms of reporting data defined in multiple taxonomies and offers several mechanisms for that purpose, in particular:

-

Separate documents for multiple taxonomies – approach where for each taxonomy, a data collector will receive a single report containing only the data that is defined by that taxonomy. Similarly, data for each taxonomy must be extracted from each individual report.

-

Multiple taxonomy references – an approach whereby a report includes references to multiple taxonomies. A data collector will receive a single report containing facts that use concepts from those different taxonomies.

-

Multiple target documents – a feature of Inline XBRL2 that allows the XBRL data in an Inline XBRL report to be segregated into multiple XBRL reports (or "target documents"). When XBRL data is extracted from the Inline XBRL report, facts are separated into multiple XBRL reports, each referencing a different taxonomy.

-

Unifying extensions – this approach allows data collectors and taxonomy authors to combine a number of base taxonomies within a single taxonomy extension to be used by preparers in order to create a single report containing data from those multiple base taxonomies.

The primary differences between these approaches are:

- Where entity-specific extension taxonomies are allowed.

- How many explicitly separate XBRL reports are produced after conversion from Inline XBRL.

- How overlapping content is handled.

- The balance of necessary complexity between the producer, collector and consumer.

Further details, as well as characteristics and consequences of each approach are presented in the rest of this section.

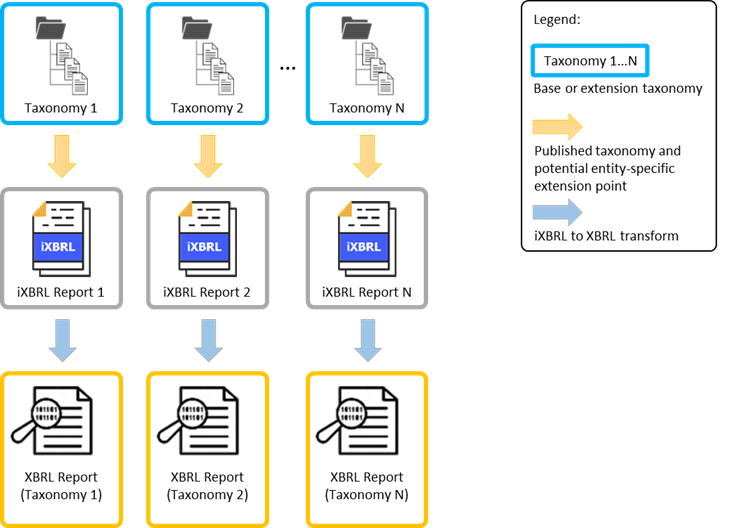

3.1 Separate documents for multiple taxonomies

The most common and basic approach observed across major XBRL implementations globally is that, for each taxonomy made available by a data collector, a single report is expected from a filer and will contain only the data relating to that taxonomy.

Using this approach for reporting multiple different topics contained in a single report, such as those found in an annual report, is possible. However, it is burdensome for preparers as it requires preparing separate reports to meet different filing obligations.

Figure 1 summarises this approach.

Figure 1: Separate documents for multiple taxonomies

Figure 1: Separate documents for multiple taxonomiesCharacteristics and consequences of this approach are:

- If the data requirements for the different reports overlap, then preparers will have to separately tag and report this data multiple times. This increases the overall effort and resources needed to produce these reports.

- When reports are created separately, it is more likely that the data in the reports is inconsistent, even in cases where there is no specific data overlap. This may be due to human error, different processes used in preparation or simply the time when each is prepared. The consequence of this is that additional reconciliation effort is required by the data collector to handle duplicated, contradicting or misaligned data. In turn, this may lead to the need for additional clarification or resubmissions from the preparers.

- Reports, data collections, filing rules and data collectors are entirely independent from each other which simplifies governance of the taxonomy and can simplify the individual data collections.

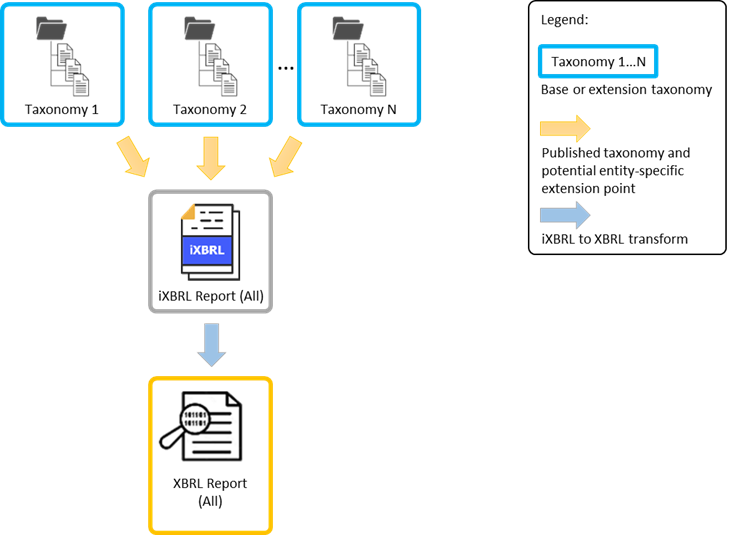

3.2 Multiple taxonomy references

All Inline XBRL (and XBRL) reports includes a reference to the taxonomy that they are prepared against. It is possible for a report to include more than one such reference, in which case the report is prepared against the combination of all referenced taxonomies.

This section describes the approach of using multiple taxonomy references in order to create a single XBRL or Inline XBRL report that meets multiple filing requirements.```

Figure 2 summarises this approach.

Figure 2: Multiple taxonomy references

Figure 2: Multiple taxonomy referencesCharacteristics and consequences of this approach are:

- Data defined in multiple taxonomies can be captured in a single report. This means:

- Inline XBRL multi-tagging (tagging the same piece of information multiple times) can be used to ensure there are no discrepancies when the same data appears in more than one taxonomy – it will be the exact same data.

- Preparing a single document leads to more streamlined reporting of multiple topics.

- Less effort is required from the data collectors to reconcile the data between the otherwise separate reports.

- The transform of a (formatted) Inline XBRL document into a (pure data) XBRL document results in a single document which contains the same set of taxonomy references as the original report. This retains the context in which the data was transmitted, but will need further processing if the data is to be split by taxonomy.

- Since the taxonomies are used unchanged, this approach does not address the general problem of overlapping definitions across multiple taxonomies. This means that preparers will need to multi-tag certain disclosures, once for each taxonomy in which the disclosure is defined. Although the total amount of tagging over the “separate document” approach is unchanged, this can be a source of errors.

- If multiple data collectors are involved, then, from the point of view of an individual data collector, a filing may contain irrelevant and unrequested information. Filing rules must allow for this case and data collectors may be expected to have some sensitivity to the multiple uses of the report.

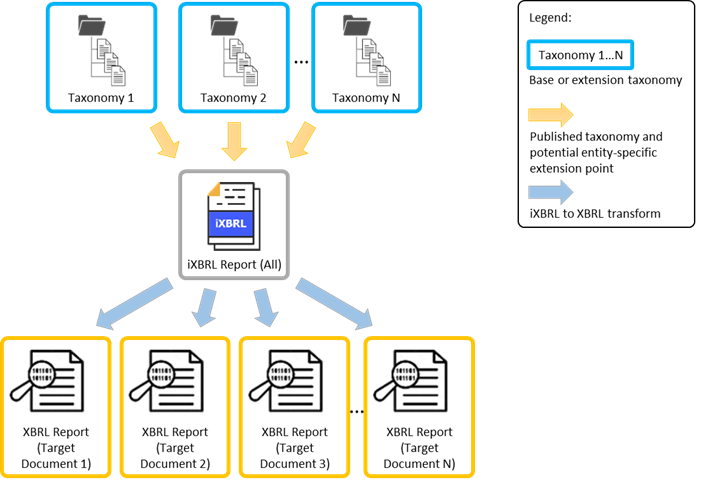

3.3 Multiple target documents

Multiple target documents refers to a feature included in the Inline XBRL specification whereby each fact in an Inline XBRL report is associated with a target document. This information is used during the Inline XBRL to XBRL transformation to create a separate XBRL report for each target document, each with its own taxonomy references. The use of target documents enables the separation of data in the Inline XBRL report so that it can be used for multiple purposes and directed to different audiences.

Figure 3 summarises this approach.

Figure 3: Multiple target documents

Figure 3: Multiple target documentsCharacteristics and consequences of this approach are:

- The ability to direct any fact into any output report allows a single Inline XBRL report to contain multiple reports. Consumers are expected to extract only the target document(s) that relates to their needs.

- Distinguishing multiple topics based on the target documents is relatively easy as there will be separate outputs provided after transformation. However, recognizing a relevant topic from the perspective of human-readable layer of the report can be challenging if it is not clearly presented in the report.

- In terms of the resultant data, multiple targets documents remove the problem of overlapping information retrieved by data consumers and does not require further reconciliation efforts.

- Each taxonomy can be used as-is without extensions by data collectors. This means respective taxonomies can properly match the specific legislation or set of reporting requirements without the need of modularizing them based on the covered topics.

- However, the complexity of reporting using multiple taxonomies in a single report is shifted from taxonomy authors to preparers, which increases the effort to prepare a final report, but not to the same extent as producing multiple separate documents. If the scope of taxonomies used in the report overlaps, no additional effort is required by data consumers, although facts will need to be tagged multiple times to ensure that each target report could be considered as complete for a given filing programme.

- Multiple target documents may also be challenging in scenarios where more than one of the base taxonomies could be extended by the preparers. This is because filer extension elements will also have to be aligned to specific taxonomies, potentially giving multiple extension taxonomies. In these cases, this option may be considered to place too much complexity with the report preparers.

- If multiple data collectors are involved, then, from the point of view of an individual data collector, a filing may contain irrelevant and unrequested information. Filing rules must allow for this case and data collectors may be expected to have some sensitivity to the multiple uses of the report.

- Unlike other approaches, the data can be split even if there is only one taxonomy used.

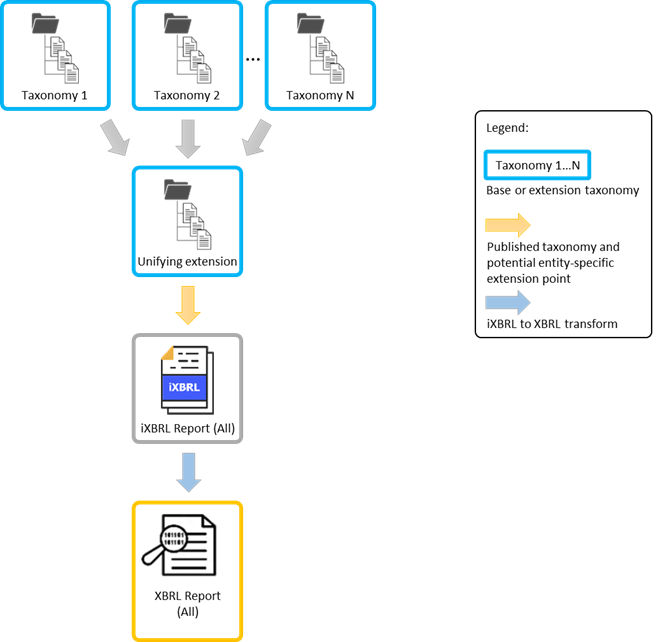

3.4 Unifying extensions by data collectors

The approach of unifying extensions introduces an intermediary step for data collectors whose requirements are defined in separate taxonomies. Using this approach, data collectors merge two or more taxonomies and introduce relevant refinements and amendments, such as removing duplicates or adding new elements, to ensure they are fit for purpose for a specific reporting programme, as well as to ensure technical consistency of the output.

The unifying extension should then offer a set of dedicated, combined entry points linking the reporting templates and elements that are relevant for different types of companies preparing the reports.

Figure 4 summarises this approach.

Figure 4: Unifying extensions by data collectors

Figure 4: Unifying extensions by data collectorsThe characteristics and consequences of this approach are:

- By creating a unifying extension, the taxonomy author who merges the taxonomies becomes the owner of the merged taxonomy. This clear ownership may be beneficial to the filing programme in general as it clarifies where the responsibility for the taxonomy in a particular reporting programme lies.

- The unifying extension can be used by data collectors to augment and adjust the original taxonomies. Importantly, this means the data collector can remove data overlaps between the different taxonomies which removes the need for reconciling the data by consumers.

- Processing the Inline XBRL report will lead to data in a single XBRL report. The lack of multiple target documents may prove burdensome, especially for data collectors with several consumers (for example, different departments of a single collecting body), interested only in certain parts of the report.

- If multiple topics are covered in a single report, it may be difficult to distinguish relevant content and ignore data which is not relevant to a given consumer.

- The underlying taxonomies are often owned by different authorities or standard setters and are subject to changes driven by forces external to the data collector. To handle this, the authors of such extensions need to take into consideration the potential needs of managing changes. This may mean adapting their governance processes and release cycles to reflect those used by the base taxonomies in scope.

- When entity-specific extensions are required, the extensions are made from the unified extension point. Having a single extension point is the simplest case for preparers. However, if it is important to be able to associate extension elements with a specific base taxonomy, there is no direct link and the relationship would need to be implied through the use of the presentation linkbase or anchoring and suitable filing rules.

- In the case of multiple data collectors being involved, then filing rules must be managed between the data collectors to ensure that using the unified extension does not make the report invalid according to any set of filing rules involved.

3.5 Mixed approach

The approaches discussed above are considered as standalone technical mechanisms capable of handling multiple taxonomies in a report. Data collectors, however, may decide on combining them to better address their requirements.

For example:

- Multiple target documents and multiple taxonomy reference approaches were combined by the Danish Business Authority (Erhversstyrelsen)

- A unifying extension (albeit with only one base taxonomy) and multiple target documents are used in the UK for listed companies so that they can use a single report for European and domestic purposes (Financial Reporting Council)

4 Comparison of approaches

The table below shows the main differences between the approaches presented.

| Approach → Area ↓ | Separate documents | Unified taxonomy extension | Multiple target documents | Multiple taxonomy references |

|---|---|---|---|---|

| Potential entity specific extension points |

One per report (per taxonomy) |

One for the whole report |

One per taxonomy |

One per taxonomy |

| XBRL reports after applying Inline XBRL transform |

One XBRL report per Inline XBRL report |

One XBRL report |

One XBRL report |

One per target document |

| Handling of overlapping content |

No handling |

Removed in extension taxonomy |

Multi-tags |

Multi-tags |

| Who handles the necessary complexity |

Data preparers and consumers |

Data collector |

Data preparers |

Data preparers |

| Filing rules |

Filing rules are independent for each taxonomy |

Single set of filing rules for data collector |

Filing rules for each collector must allow this approach |

Filing rules for each collector must allow this approach |

5 Summary of recommendations

If multiple taxonomies are required for a company to meet its filing obligation, then it is recommended that the data collector creates a unifying extension. In doing so, a single taxonomy is published where overlaps in data points are resolved and it is still amenable to extensions. This is the approach that is considered to most reduce the filer burden and collect the most unambiguous and useful data.

While this guidance is clear in its recommendation, it is acknowledged that legislative, technical and governance related items may prevent the unification of taxonomies in this way. In these cases, the multiple target document approach is recommended as an alternative. It should be noted, however, that all approaches presented here achieve the overall goal of reporting against multiple taxonomies and may be the best choice for a specific filing programme.

- Data collectors should prefer to use a unifying taxonomy extension

This document was produced by the Taxonomy Design Working Group.

Published on 2024-10-02.